Fractional Ownership, Lottery Savings & Vaccines as Startup Investments

This week we start with a look at fractional ownership of assets before discussing what the possible implications of this growing trend are. Next, we take a look at a startup using a clever psychological trick to encourage people to save more money. Finally, a piece on how the federal government is taking on the role of a venture capital firm with respect to vaccine development.

Fractional Ownership (2 min)

Lottery Savings (1 min)

Vaccines as Startup Investments (2 min)

What effect do fractional shares have on stocks and markets more generally?

Fractional shares allow investors to buy into companies at dollar amounts other than a multiple of the current price per share in the market. They're commonly used by investors who want to own equity in a company with a relatively expensive share price (eg: Amazon @ $3100/share or Berkshire Hathaway Class A @ $327,000/share) but who either can't or don't want to invest the full amount to buy one share. Instead, an investor with $100 can utilize fractional share trading from their brokerage to get 3.2% of an Amazon share (or .03% of a share of Berkshire Hathaway) instead of being stuck only being able to invest in companies with share prices below $100.

Behind the scenes of fractional share trading are the brokerages (Fidelity, Schwab, or Robinhood) who offer the service to retail investors. If Alice wants to purchase $100 of Amazon stock then Fidelity will actually be purchasing 1 entire share of Amazon and giving Alice custody of 3.2% of it. Fidelity will own the other 96.8% until they can find other customers who are looking to buy portions of Amazon. If the next day Alice decides to sell her portion of Amazon stock then Fidelity will give her the current market price for her portion of the share (3.2%) and attempt to match her order with another customer who wants to purchase a fractional portion of Amazon (If they can't find a match then they'll assume the risk of the price moving against them on the share). With enough customers and demand for fractional shares (we call this liquidity) they're able to minimize their exposure to price movements in the equities they're offering and offer fractional trading as a service without adding significant amounts of volatility to their bottom line.

As fractional trading becomes more popular (and cheaper) I think it's likely that we'll see a shift towards people creating their own indices (or "baskets") of companies that they want to invest in. More specifically I think it's likely that people will start to identify companies that they do not want to invest in and will prefer to choose an existing index and subtract companies from it. For example, if Diego wants to invest $1000 in an index fund of U.S. companies but is also climate-conscious he might want to remove Exxon Mobile, Chevron, and ConocoPhillips from his index (thereby creating his own index with fractional shares and distributing his $1000 appropriately). This level of customization is currently out of reach for the average retail investor but will certainly be possible in the near future.

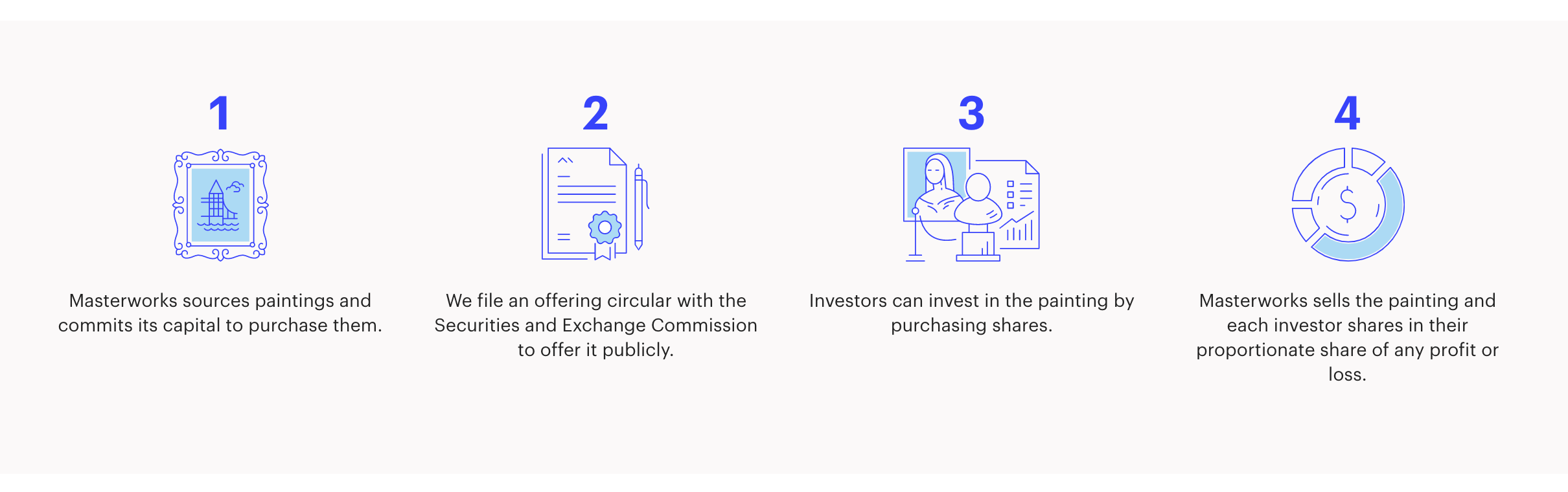

Fractional investing/ownership doesn't just have implications for investors in the equities markets. Platforms like Masterworks and Mythic Markets allow investors to have stakes in art and other collectible markets as well.

In fact, the winner of this year’s Kentucky Derby (a horse named Authentic) is actually part-owned by investors on MyRacehorse. As the demand for access to investments traditionally reserved for those with large amounts of capital grows, fractional ownership seems poised to grow in importance. It's not hard to imagine a future where you don't own just one horse or one piece of art but instead can buy into an index of all horses of a certain breed or an artist's entire collection of works.

In Other Words

Fractional ownership involves one entity purchasing an asset and assigning partial custody to an individual (or group of individuals) who wishes to own a portion of the asset. We've seen examples of this with stocks, art, horses, and even housing. Since we're at the beginning stages of this type of novel ownership structure existing, I think that we'll soon see new financial products and investment strategies that take advantage of the lower barrier to entry and allow people to invest in asset classes they never would have considered before.

Will turning savings accounts into a prize-linked lottery cause people to save more money?

A startup called Yotta Savings recently launched a savings accounts with one single modification. Instead of paying their user's interest on the money in their savings account, they're paying users in the form of a lottery (whose math works out such that users on average earn about the same level of interest, or APR, as a traditional savings account). "For every $25 held in Yotta Savings account, you get 1 lottery ticket every week. A lottery ticket has 7 numbers. Everyday, one random number is drawn. At the end of the week you win prize money depending on how many numbers on your ticket matched with the numbers that were drawn. The prize ranges from $0.10 to $10 million." It's a clever piece of financial psychology that should cause people to save more money in the hopes of winning a big prize.

It's also not an entirely new model. Prize-Linked Savings accounts are offered by banks in many states across the U.S. They are most popular in Iran, where many savings accounts are actually paid out through a method like this because traditional forms of guaranteed interest are banned by Islamic law.

It seems that there's a growing trend of apps that exist to disguise saving money in different ways. Another popular vein of applications (Acorns being the biggest) utilizes a technique called round-up saving whereby every transaction you make is rounded up to the nearest whole dollar with the difference in round-up being deposited automatically in a savings account.

On one hand, it seems like we are moving towards a society with ever more empowerment for the individual investor where we're democratizing access to assets and asset classes through concepts like fractional ownership. And yet, simultaneously these savings products show us that we still have trouble with basic financial literacy and setting money aside.

In Other Words

Prize-Linked Savings accounts pay users in the form of a variable reward (differing amounts of money awarded on a recurring basis) that ends up being mathematically designed to give out the same amount of money as people would have earned by parking their money in a regular savings account. The excitement around the lottery system seems to work and encourage people who sign up to save more.

Why is the U.S. investing in so many vaccines when some of them are clearly not going to work?

To date, the U.S. government has committed over $5 billion to vaccines from the following companies: Pfizer, AstraZeneca, Johnson & Johnson, Moderna, Novavax, Merck, Sanofi, and others. There's no doubt that billions of these dollars will ultimately prove futile as some of the vaccines under production fail to work or demonstrate efficacy.

But as long as the money directly or indirectly helps in the development of a successful vaccine then I think it's fair to say that the government has not made bad decisions on how to allocate funding. One of the most famous quotes in marketing is: "Half the money I spend on advertising is wasted; the trouble is I don't know which half". A more appropriate phrase for vaccine development from the government's perspective might be: "Half (or more of) the money I spend on vaccines is wasted; and I don't care which half it is, as long as there is a vaccine". After all the benefit from successfully finding a vaccine will be worth orders of magnitude more to the economy (we’ve already allocated an extra $3 trillion to shore up the economy), population, and world than the few billion that's put into efforts that don't end up working.

Paradoxically, because the government does not have perfect foresight when it comes to knowing which vaccine under development will ultimately prove successful, the government's role looks similar to that of a Venture Capital firm deciding which firms to invest in. As we talked about previously, some venture capitalists would benefit from simply blindly investing in all credible deals (in other words becoming index investors in startups) simply because the value of the single biggest winner is so great that missing it is catastrophic for their returns (we call this a power-law distribution). You can think of the collective investment as the government taking a short position on the status quo (virus stricken economy) and going long on economic recovery for the benefit of its citizens. Each vaccine investment is basically a lottery ticket with an immense potential payout.

As we began to analyze the government's response to the crisis, I think keeping the VC model in mind might help explain why/how money was distributed and should show that money "wasted" was really money well spent.

In Other Words

The value of a single successful vaccine far outweighs the cost of funding all credible vaccines which makes the rational government strategy one where they attempt to invest in as many as possible. This will inevitably result in billions of dollars being poured into vaccines that don't work but this should be looked at positively instead of negatively. I propose that we use the mental model of the government as a VC firm and the vaccines as startups in order to judge their success by the success of the entire cohort of vaccines instead of on an individual basis.

How satisfied were you with this week's issue?

Let me know what you think in this 3 question survey

That’s all for this week. Thanks for making it this far and I hope you found these answers as interesting to read as I found them interesting to write. If you liked what you read, feel free to share it with someone who you think will enjoy it.

As always,

Roosh → You